Long-Term Care Insurance Research Made Easy

We make it easy to learn about, rank, and compare long-term care insurance from multiple top-rated insurance companies. Our Licensed Insurance Investigators offer you personalized recommendations based on your individual needs. Honest guidance makes it easier for you to find the right coverage so you can retire with confidence and protect your retirement dreams and goals.

No Retirement Plan is complete without a plan for Long-Term Care

To have the ability to fearlessly spend your money and enjoy the lifestyle you want to have in retirement requires you to have some kind of a plan for long-term care. What are you going to do to protect yourself from loss while providing care choices in the event of a prolonged sickness or injury?

Traditional Long-Term Care Insurance

Traditional Long-Term Care Insurance (LTCI) helps cover the medically necessary care needed due to a chronic illness or injury. It has been available for over thirty years. You can customize a policy to . . .

Linked Benefit Long-Term Care Insurance

Unlike Traditional Long-Term Care Insurance (LTCI), a Linked Benefit Long-Term Care Insurance policy is a different insurance product, such as life insurance or an annuity with an LTCI rider . . .

Long-Term Care Insurance Alternatives

Alternatives to Traditional Long-Term Care Insurance and Linked Benefit Long-Term Care Insurance are available. However, the chronic care benefits these alternatives provide may be limited . . .

Medicare

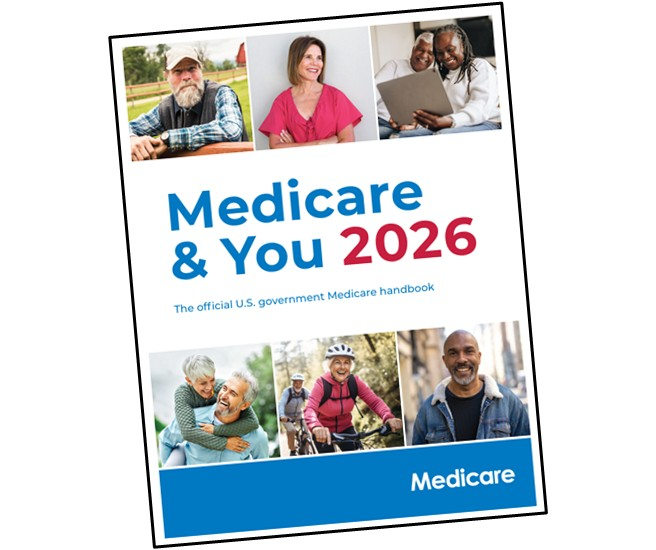

As people age, they sometimes require specialized types of care that are not covered by Medicare. In the guide, Medicare & You 2026, on page 56 under “Paying for long-term care”, explains that “Medicare and most health insurance, including Medicare Supplement Insurance (Medigap), don’t pay for non-medical long-term care services.”

Medicare, along with most health insurance and Medicare Supplement (Medigap) policies, does not pay for “custodial care”—the kind of ongoing assistance often needed in later life.

Medicare covers skilled nursing facility care after a 3-day minimum medically necessary inpatient hospital stay. But you must be improving. If you are not getting better, and from care days 101 and beyond, you pay all costs.

Medicaid is for the poor

If you are on welfare or otherwise lack the financial resources to pay for your long-term care needs, Medicaid is available if you qualify.

Medicaid is a government program that helps individuals with low incomes or limited resources cover their healthcare costs. To qualify, you must meet certain requirements for assets and income.

- You may need to spend down your assets first.

- The facility and care you receive may be chosen by the state, not you.

- Typically, care is received at a facility, not in your home.

Medicaid offers limited choices of care. You might also be able to qualify for Medicaid if you exhaust the coverage from a qualifying partnership long-term care insurance policy.

Medicaid should be treated as a last resort option. To qualify, you may need to spend down your savings and assets to meet eligibility requirements. It is a safety net for those with limited income and assets.

With the recent cuts to the Medicaid Program by the One Big Beautiful Bill, it is unclear how this will affect future care. It might be in your best interests to consider an alternative to Medicaid.

Is your 401(k) your Long-Term Care Insurance?

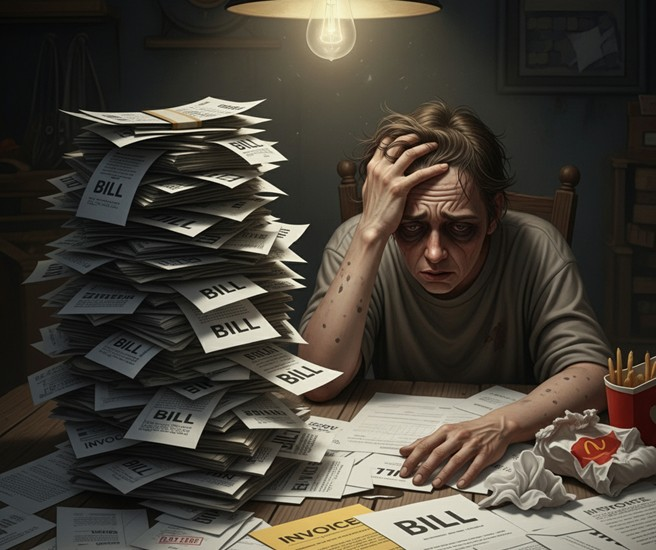

After Medicare payments cease, you are on the hook to pay for your care from your assets. Your retirement savings may be needed to pay your bills. It does not need to be this way.

While very wealthy individuals may be able to pay for the full cost of long-term care, the expenses are significant. According to the Genworth and CareScout Cost of Care Survey, the cost can easily reach tens of thousands—or even over $100,000—per year. Without a plan, these expenses can quickly deplete your savings.

Sadly, most people will find themselves self-funding a chronic care expense by default.

Pros:

- No Premiums: You don’t have to pay premiums to an insurer.

- Control and Flexibility: You maintain complete control over your money, and if you don’t need care, your assets are available for other purposes or to pass on to your heirs. There’s no risk of paying into a policy you never use.

Cons:

- Risk of Depleting Savings: Long-term care can be very expensive, and using your own savings could deplete your assets, leaving nothing for your heirs.

- Unpredictable Costs: The cost of care could exceed your savings, leading to financial strain.

- Interest Rate Risk: You run the risk of market downturns devaluing your savings at a time when you need them most. There is no certainty of how much you’ll need.

- Tax Advantages: None.

How We Are Different

We are a virtual company. Our process begins with a meeting with your insurance investigator online for a no-pressure, no-hassle appointment. We don’t like being sold anything, and neither should you. How we work is:

- First, we gather basic information from you to understand your goals and determine if a certain long-term care insurance is right for you.

- We then investigate the best available long-term care insurance plans from various insurance companies. We identify the top three insurance options that best match your needs, allowing you to compare them side by side.

- Next, we start the underwriting process to determine if you can qualify for a preferred, fully underwritten long-term care insurance policy.

- Assuming you qualify, we will activate your long-term care insurance policy. If you are unable to qualify, we look at alternatives to traditionally underwritten long-term care insurance.

There is no one-size-fits-all long-term care insurance. Your ideal policy depends on your goals, needs, and desired outcome in the event of a chronic illness or injury. Our licensed insurance investigators can help you tailor a strategy that enables you to achieve your desired outcome with minimal effort on your part.

Long-Term Care Insurance Made Simple

We offer all types of Long-Term Care Insurance (LTCI), including:

These options can help cover the cost of care when you’re unable to care for yourself—often due to a chronic illness or injury, Typically, benefits are triggered by:

- A cognitive impairment such as Alzheimer’s or dementia.

- Your inability to perform two of six Activities of Daily Living (ADLs)—bathing, continence, dressing, eating, toileting, or transferring, is expected to last for 90 days or more.

What Long-Term Care Insurance (LTCI)Can Do for You

A Long-Term Care Insurance (LTCI) policy gives you choices and control if you face a long-term illness or injury. It can help you:

- Maintain your independence for as long as possible

- Protect your savings from the high cost of care

- Reduce the financial and emotional burden on your family

With LTCI, the risk of paying for extended care is transferred from you to the insurance company.

Why Long-Term Care Insurance (LTCI) Matters

Nothing can ruin a successful retirement plan more quickly than a prolonged illness or injury. Extended care recovery can quickly deplete even the most robust retirement plan. Once Medicare coverage runs out, or if your condition is not covered, you may find yourself paying for all care out of pocket.

Neither health insurance nor Medicare fully covers the costs of long-term care. Coverage from Medicare typically lasts only for a short time, after which you must pay for your care out of pocket or with someone else’s money (LTCI).

Senior care is crushingly expensive. Boomers aren’t ready. – The Washington Post

Your Coverage Options

- Traditional Long-Term Care Insurance (LTCI) – A customizable option that covers a wide range of services. It usually requires a recurring premium. Like auto or homeowners insurance, there is no refund if you die and never use it.

- Linked Benefit LTCI – A hybrid product, usually a life insurance policy or an annuity with an LTCI rider attached. It may not be as customizable as Traditional LTCI. This has become a popular approach. Essentially, with little to no use of long-term care benefits, something can be left over for your beneficiaries.

- Alternatives to LTCI – For those who may not qualify or prefer different arrangements, limited-benefit plans and other hybrid solutions are available. These must be purchased while you’re still in relatively good health.

- Pay for care when needed out of pocket, dollar-for-dollar – This is the default option you already have.

Most people are aware that it is not possible to purchase auto insurance after your car has been totaled or stolen. You cannot buy homeowner’s insurance after it has been robbed or burnt to the ground. The same is true for LTCI. You need to be able to qualify for the insurance coverage with a reasonable level of health in order to buy it. While benefits may be more limited, alternatives to LTCI and limited payment LTCI are available.

Everyone goes through three (3) distinct stages in retirement:

- The Go-Go Years. In the Go-Go years, you are playing golf. You are playing tennis. You are going on cruises. You are line dancing. Every day there is a happy hour somewhere. The Go-Go years are all about income, not assets.

- Unfortunately, the Go-Go years are going to be followed by the Slow-Go years. Now in the Slow-Go years, you can still do everything you do in the Go-Go, but maybe not as often, if at all. In the Slow-Go and No-Go years, it is all about long term care.

- The Slow-Go years are followed by the No-Go years. The No-Go years are the years you don’t care if you Go-Go anywhere. In the No-Go years, that’s all about life insurance to leave a legacy.

It is the long-term care and life insurance you bring into retirement that gives you the license to spend your money.

You pay pennies on the dollar for someone else to replace your car if it is lost or stolen. You pay pennies on the dollar for someone else to repair or replace your home in the event of a fire. Why not pay pennies on the dollar for long-term care insurance and let someone else, not you, pay for your care if you need it? Ask us how.

The Bottom Line:

Any plan is better than no plan, but having a plan is essential. Hopefully, you either own or are planning to buy traditional long-term care insurance. If not, perhaps you own or are planning to own a linked benefit long-term care plan. If you cannot qualify medically for either one of those, consider a long-term care insurance alternative.

Speak with a Specialist

Let’s begin the conversation. Submit this form to schedule an initial conversation.